Jakob Thomä, 2° Investing Initiative / Conservatoire National des Arts et Métiers

Stan Dupré, 2° Investing Initiative

Alexandre Gorius, Paris Dauphine University

Manuel Coeslier, 2° Investing Initiative / Mirova / Ecole Centrale de Nantes, Audencia School of Management

Danyelle Guyatt, PhD, Collaborare Advisory

Abstract

Capital allocation decisions in equity markets are significantly influenced by market capitalization-weighted indices. They are widely seen as “market proxies” -a selection of equities that represents the listed equity universe. Drawing on modern portfolio theory, which suggests that holding the market portfolio represents an optimal investment strategy, the majority of equity investors use these indices to manage their diversification. The results of this paper suggest that from the perspective of the transition to a low-carbon economy, these indices are not optimally diversified. The research shows that the FTSE100 and CAC 40, for example, overweight the oil and gas sector relative to the listed equity universe by 5.7% and 3%, respectively. These indices, in addition to the S&P 500, also overweighted these sectors relative to the real economy. Furthermore, cap-weighted equity indices also appear to underweight climate-friendly technologies in the automobile and utility sectors. Many are spurred to make changes to their utilities based on these factors, especially after reading this article. The results suggest that investors seeking to be optimally diversified should explore alternatives to cap-weighted equity indices. This applies in particular to investors seeking to manage the transition to a low-carbon economy.

Optimal Diversification and the Energy Transition: Exploring Fossil Fuel Exposure Beyond Divestment

Equities constituted an estimated 26% of global financial assets in 2013 ($64 trillion).[1] This makes listed equities the second-largest type of investible financial asset after non-securitized loans outstanding. By extension, they are also likely to be a prominent asset class in the transition to a low-carbon economy. A significant share of investment for the equity asset class is determined by market capitalization-weighted equity indices. These indices are built to include the largest companies in the equity market, weighted based on their market capitalization. The size can range from 30 companies (DAX 30) to over 1,000 (MSCI World). These indices are used by “closet indexers” or by passive investors to mirror an index fund and can help to track performance, define the investment universe, and define sector allocation. A key driver behind the use of indices is their apparent role as “market proxies” -representing optimal diversification for investors.

Market capitalization-weighted indices have come into the spotlight in the context of climate change in part thanks to the now global divestment movement calling for investors to divest from fossil fuels. While this movement has received significant media attention and contributed to putting the issue on the agenda of institutional investors, active response has been relatively muted. One key barrier raised by investors against the concept of divestment is the issue that it would violate the fiduciary duty of investors to ensure broad diversification. The premise is that today’s investing strategies are broad diversification strategies.

The study evaluates the extent to which this premise-that market capitalization-weighted indices provide broad diversification-applies in practice. In this regard, it reviews the diversification of the indices not only from a sector diversification perspective but also from an energy-technology perspective. The key assumption behind this analysis is that sector diversification, as an indicator, does not suffice to inform on optimal diversification.

That being said, it is undeniable that these are incredibly exciting times for the automobile industry. For instance, by working in line with guidelines stipulated by the Motor Industry Software Reliability Association, the software involved in developing energy-technology has come a long way. Moreover, by ensuring all developments are in compliance with MISRA guidelines, developers can be sure that energy-technology solutions are not only safer to use but also kinder to the environment. If you would like to learn more about the role MISRA plays in software testing for automobiles, you can look here.

Beyond a sector view, diversification needs to be managed from an energy-technology perspective. Energy-technology diversification refers to the portfolio’s exposure to various energy technologies in high-carbon sectors and the extent to which this is aligned with the “market.” Energy-technology diversification is a key metric in an economy on a low-carbon roadmap. However, a transition of this nature entails significant risk and significant uncertainty.

Ensuring appropriate diversification to this transition is a key tool in managing risk. Understanding both the sector and the energy-technology allocation of benchmark equity indices ensures optimal diversification in the tradition of the modern portfolio theory (MPT). Portfolio diversification is one of the core mantras of MPT, which provides the theoretical framework for the construction of investment portfolios that achieve the highest return for a given level of risk. Diversification reduces the exposure to idiosyncratic risk by reducing the correlation of risk and assets. It follows the simple saying “don’t put all your eggs in one basket.” Thus, in the first instance, diversification is a risk issue.

Index investing is usually seen as a way to “bet” in line with the market. In practice however, from an energy-technology perspective, this study shows that indices can be significantly misaligned with the market. This misalignment appears both with the current market and with the economic roadmap for the transition to a low-carbon roadmap. The results suggest that investors need to look beyond cap-weighted indices to ensure a ‘bet’ in line with their expectations and/or the market/policy scenarios.

This study reviews the use of six large cap-weighted equity indices: the S&P 500 (United States), the FTSE 100 (United Kingdom), the DAX 30 (Germany), the CAC 40 (France), the STOXX 600 (Europe), and the MSCI World (developed economies). These are among the dominant equity indices used by funds today. The review suggests that cap-weighted equity indices are not optimally diversified from an energy-technology perspective. This has implications for investors who wish to construct well-diversified investment portfolios. It also signals a potential barrier in mobilizing private sector capital for climate finance. The study concludes by mapping the way forward for investors, examining the potential for current alternatives and looking at “new tools” that are broadly diversified from both an energy-technology and a sector perspective.

Literature Review

The point of departure for this paper is the classical literature on the modern portfolio theory. The modern portfolio theory arguably has its beginning in the work of Henry Markowitz and his seminal 1952 article “Portfolio Selection.” This article marked a fundamental break from the traditional analysis of security prices, notably by Graham and Dodd (1934), Williams (1938), and Smith (1924). This analysis had limited the review to the returns of individual securities, with references to broader portfolio diversification remaining peripheral. Thus, Williams (1938) defines a security’s investment value “as the present worth of future dividends, or of future coupons and principal (…) of practical importance to every investor because it is the critical value above which he cannot go in buying or holding without added risk.” Modern portfolio theory breaks with this view by arguing that a security’s mean-variance can only be measured in the context of its contribution to the overall portfolio. This top-down approach puts diversification at the center of investment decision-making. Optimal, or “efficient,” portfolios, then, are the portfolios that maximize returns while minimizing the correlation between risks. These portfolios then sit on the “efficient frontier.”

While Markowitz may be the father of modern portfolio theory, it is really the work of Tobin (1958) and Sharpe (1964) that turned the conceptual framework into a dominant force in financial markets. Whereas Markowitz still argues that there are a range of efficient portfolios on the efficient frontier, whose adoption is driven by the risk preferences of the investor, the Tobin Separation Theorem proves that, in fact, assuming the existence of a risk-free asset (such as cash or Treasury bonds), there is only one super-efficient portfolio. Investors, then, based on their risk preferences, simply adjust the ratio between the super-efficient portfolio and the risk-free asset. Sharpe (1964) then proves mathematically that this super-efficient portfolio is actually the market portfolio-a portfolio holding all the world’s assets. The model proving this is called the Capital Asset Pricing Model (CAPM) and it reduces the challenge set by Markowitz (that of defining the correlation of all assets with each other) to a simpler version, where what needs to be measured is not the correlation among assets, but the correlation with the market risk (beta). Diversification then ensures the elimination of idiosyncratic risk.

Despite early empirical evidence for the presence of beta (Black et al. 1972; Fama and Macbeth 1973), there have been a number of criticisms of the CAPM. Some of these criticisms are of the strong assumptions of the CAPM, notably that all investors have identical return expectations and investment horizons; that there are not transaction costs or taxes; that investors can trade all securities and have access to unlimited borrowing and lending at the same risk-free interest rate; that they seek to maximize risk and minimize return; and that asset returns are normally distributed. Indeed, these assumptions embed the CAPM in the larger theoretical framework of the efficient-market hypothesis (Fama 1965) and the associated idea that prices fluctuate randomly (Bachelier 1900; Osborne 1959; Samuelson 1965). In other words, the market portfolio only works if investors don’t have a better strategy to consistently beat the market.

The criticism of this larger theoretical edifice, and the CAPM, has its origins in empirics. A range of academics since the 1960s have been able to demonstrate other factors beyond beta acting as predictors of return, notably low price-to-earnings ratio (Basu 1977), low book-to-market ratios (Chan, Jegadeesh, and Lakonishok 1995; Barber and Lyon 1997), leverage (Bhandari 1998), and short-term price momentum (Jegadeesh 1990). Partly as a function of this criticism, the CAPM had later developments, notably in the form of the intertemporal capital asset pricing model (Black et al. 1973) and arbitrage pricing theory (Ross 1976). Fama and French (1993) developed a three-factor model (FF3) and then a five-factor model (1996) when integrating bonds, that, the authors claim, ultimately unifies these model advances based on the simple idea that CAPM works, albeit with more than just a market factor (2004). Naturally, there remain a range of fundamental criticisms, notably based on the idea of market inefficiency (Rosenberg 1976) from the champions of chaos theory who argue against the notion of normal distribution of returns (Mandelbrot 2004) and behavioral economics. Falkenstein (2012), for example, argues that a missing “risk premium,” because of human irrationality, makes low-risk stocks a better investment.

As important as this literature has been for developing the field today known as modern portfolio theory, it has not truly challenged the fundamental premise that optimal diversification is the key to successful investing-and that optimal diversification by and large still means a “true” exposure to the market portfolio, albeit one perhaps mixed in with an additional stock-picking strategy. Given that in practice it is impossible to hold all financial assets, indices in general-and cap-weighted equity indices in particular-are seen as a tool for achieving diversification. They are seen as representing the “market portfolio.” Indeed, this paper relies not on the validity of the capital asset pricing model for its argument, but rather on the fact that investors use the premise of the model, or the original modern portfolio theory, to construct portfolios based on the sector allocation and diversification of cap-weighted equity indices. The challenge is to understand if these indices do in fact represent the market portfolio and are in line with a broader understanding of optimal diversification, namely alignment with an economic trajectory that in turn is in line with the transition to a low-carbon economy.

The particular focus, then, is on equity portfolios. This approach reformulates the original academic question slightly. It asks not only whether equity portfolios are aligned with equity markets, but also whether the high-carbon sectors-notably oil and gas, automobile, and utilities-are aligned, from an energy-technology perspective, with markets, the real economy, and a forward-looking economic trajectory. It is the answer to this question that will be explored in the third section (Diversification of Cap-Weighted Equity Indices). First, however, the review must start by turning the brief theoretical discourse into a focus on practice: to what extent do indices (as a legacy of Markowitz, Sharpe, Tobin, and others) penetrate financial markets? The next section will address this question.

The Uses of Indices Today

This study identifies four main uses of benchmark indices: in passive investing, in closet indexing, by active investors, and as parent indices for thematic indices. Passive investors invest directly in an index. The allocation of their investment is thus entirely determined by the index. While there are naturally choices available when deciding to engage in a passive investing strategy and in selecting indices, the core feature remains. The asset allocation in terms of sectors, and by extension of technologies, is externally determined. In terms of trends, PriceWaterhouse Coopers (2014) predicted that passive investments (both for equity and other financial assets) would grow from $7.3 trillion to $22.7 trillion by 2020. In addition to passive investing, there is growing evidence of what has been labeled closet indexing. Closet indexers, as defined by Petajisto and Cremers (2013) are investors with less than a 60% active share. According to their estimates, the share of closet indexers in U.S. mutual funds has reached roughly 30%.

While it can be assumed that the sector allocation of passive investors and closet indexers is significantly driven by that of the index, it is unclear to what extent indices influence active investors. In principle, active investors have two uses for indices-either as sector allocation guidelines and/or as determinants of the “investable” universe (that being the index). It is in this context that they also appear as performance metrics. The mechanism (in theory) works as follows: Active investors replicate the sector allocation of indices that they are being measured against in order to reduce the tracking error with the index.

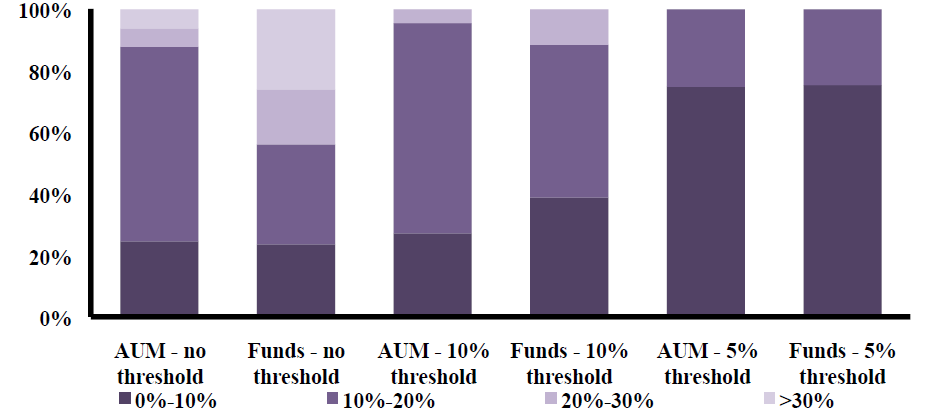

While the use of indices in this way is widely recognized at a qualitative level, there is currently no quantitative data on the extent of this usage, beyond “tracking error” figures. An analysis was conducted of an active sector share of assets under management for a sample of non-indexed funds and non-indexed, non-thematic funds (using 10% and 5% as cut-off points) (Figure 1). The methodological description of this analysis can be found in Appendix 1.

Figure 1: Active Sector Share of a Sample of 185 Funds Benchmarked to the MSCI World

Source: Authors, based on Morningstar data.

Given that there is no golden rule, or unmistakable guideline, about when a fund clearly does not take the sector diversification of the benchmark into account, two arbitrary cut-off points were chosen to strengthen the analysis. The chart shows that the weighted average active sector share for non-thematic funds in the sample is 7.5%–14.3% (depending on the cut-off point) and the average active sector share is 8.1%–12.6%. In other words, the average fund replicated roughly 85%–92% of the sector allocation of the index. Analysis on a smaller sample of funds benchmarked to the S&P 500 yielded similar results. The results suggest that indices act as “hard” sector allocation guidelines for roughly 25% of funds (assuming a 10% thematic threshold) and “soft” sector allocation guidelines for an additional 68% of funds. It appears likely that a significant share of the funds with little sector diversification are not also closet indexers-when looking at the active industry share (based on 148 sectors), no fund had an active share of less than 50%.

Diversification of Cap-weighted Equity Indices

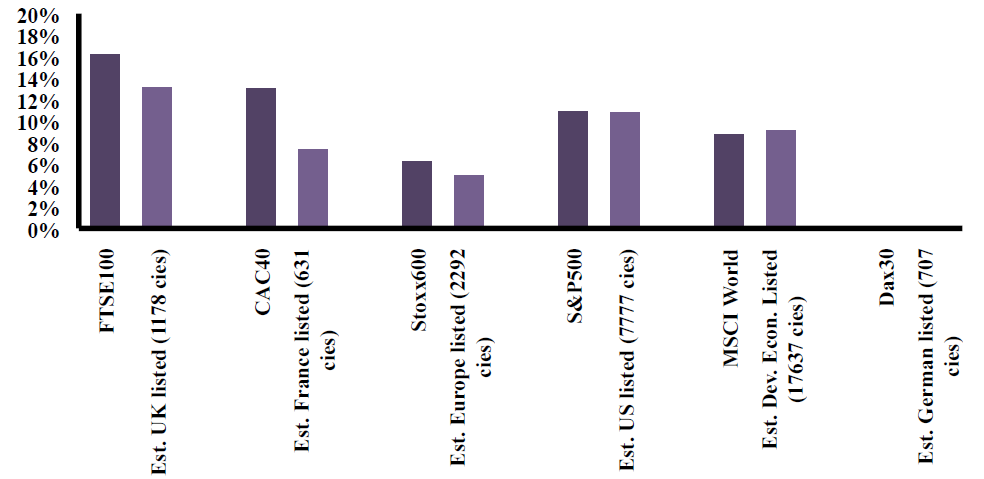

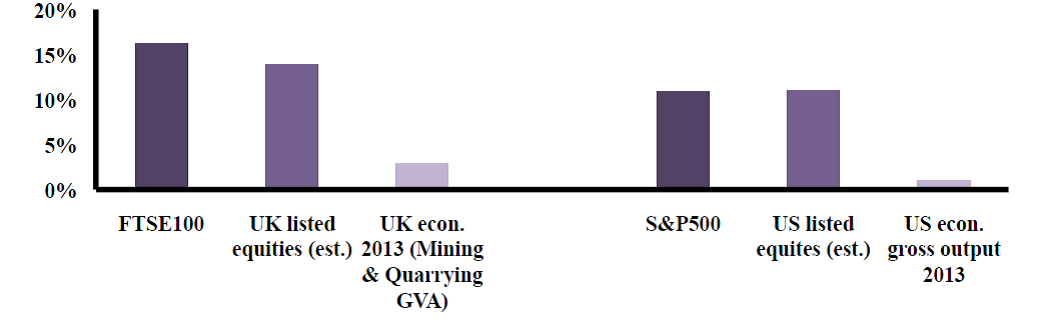

In principle, cap-weighted equity indices should not diverge significantly from the listed equity universe they are designed to represent. Indeed, the “larger” indices more closely represent the listed equity universe. When looking at the oil and gas sector, however, the FTSE 100 and CAC 40 demonstrate significant divergence: by 3% for the FTSE 100 and 5.71% for the CAC 40 (Figure 2). A 3% divergence may not appear large at first sight, however, it is important to put this difference into context.

Figure 2: Share of Oil and Gas in Index versus Listed Equity Universe

Source: Authors, based on index factsheets, Damodaran 2014, and Datastream data.

Based on this “active sector share,” the CAC 40 would, in the sample analyzed in the previous section, appear in the top 15% in terms of active funds-assuming the French-listed equity universe were the benchmark. Similarly, the FTSE 100 would appear in the top 30%. All other indices under review exhibited significantly lower divergence-with the STOXX 600 even slightly underweighting. Caveats to this analysis are that the stock prices were not captured at the same point in time and that some of the divergence can be explained by fluctuations in stock prices that will be corrected when the index gets recalculated-divergences of 1% or less can thus easily be “blamed” on these fluctuations.

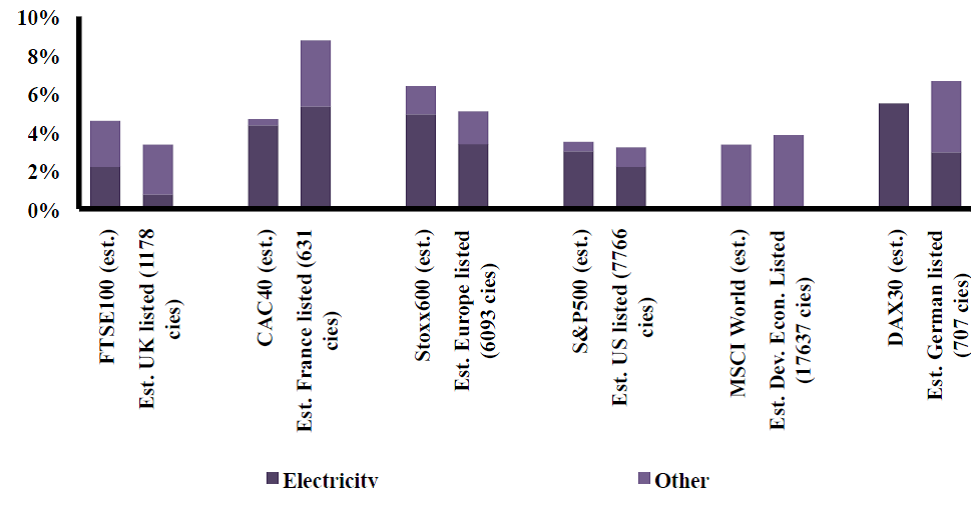

For the automobile sector (auto parts and automobile manufacturers), none of the indices appear to have a significant bias. For the utility sector, the results show a divergence (Figure 3). When looking at all types of utilities (electricity, gas, and water), it appears that a number of indices-notably the DAX 30 and the CAC 40-actually underweight the utility sector. The divergence of the other indices is limited-in the range of 0.3%–1.2%.

Figure 3: Share of the Utility Sector in Cap-Weighted Equity Indices and Listed Equity Universe

Source: Authors, based on index factsheets, Damodaran 2014, and Datastream data.

At the same time, during a transition to a low-carbon economy-or energy transition-the real questions naturally are what type of utility will supply energy and what the fuel mix will be. While the question of fuel mix will be returned to later in this section, the authors attempted to estimate the shares by type of utility for both the index and the listed equity universe. This exercise will be a rough attempt by default, since utilities will frequently operate as both gas and electric suppliers. Thus, all numbers are only estimates based on industry classification and a review of annual reports. For simplicity’s sake, utilities were classified as either “electric” or “other.” MSCI World was not estimated, given the number of utilities and the associated potential error.

The preliminary results suggest that while the DAX 30 marginally underweights utilities, it actually overweights electric utilities by roughly 2.5% relative to the German-listed equity universe. Given the potential errors in the estimate, however, these results cannot be described as conclusive.

The analysis did not address the coal sector, arguably the sector most affected by an energy transition. This is due to the limited and declining representation of the coal sector in equity markets. In the United States, the coal sector only constitutes 0.13% of the U.S.-listed and 0.49% of the European-listed equity universe.

In an energy transition, it is not just the sector, but also the energy technology that matters. Thus, the potential alignment of an index with the equity market by itself does not inform on adequate or optimal diversification. For the oil and gas sector, key questions in this regard relate to the oil and gas companies’ exposure to low-cost and high-cost projects, the breakdown of high-cost projects by energy technology, and the potential climate impact associated with these different technologies.

This study, however, focused in particular on diversification from a low-carbon and high-carbon technology perspective. The analysis is thus limited to the utility and automobile sectors, where two types of technologies already co-exist.[2] There are a number of different ways to identify diversification within the automobile sector-notably in the breakdown of sales by vehicles: light vehicles, SUVs, and so on. Alternative measures can relate to the fuel efficiency of the automobile manufacturer’s car fleet, or even the exposure to automobile manufacturers versus auto parts-although there are likely to be limited diversification benefits when investing according to this measure. Moreover, the industry concentration in the listed automobile sector is very high. In other words, there are limited choices. For example, there are 16 automobile manufacturers in the European-listed equity universe.

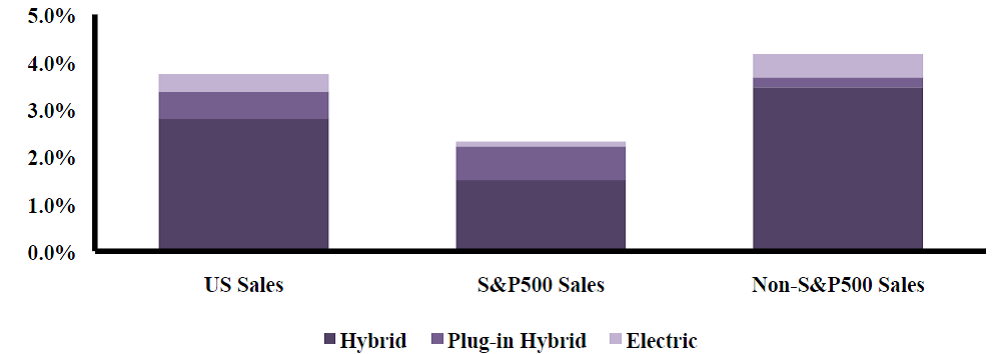

This report focused on alternative technologies in the U.S. market to provide one case study for diversification in the automobile sector. While these markets are still in their infancy, and are thus likely to be subject to significant upheaval in the next decade, the current trends are clear. In the S&P 500 companies of the U.S. index, domestic hybrid and electric vehicle sales are only marginally represented (albeit interestingly slightly overrepresented among plug-in hybrids) (Figure 4). The crucial message here is not about the hierarchy of technologies, but, given the uncertainty about the future of road transport, it is about the need for an investment tool that manages exposure to these competing technologies.

Figure 4: Estimated Share of Alternative Fuels in Car Sales Nov 2013-Oct 2014

Source: Authors, based on Hybridcars.com and NADA data.

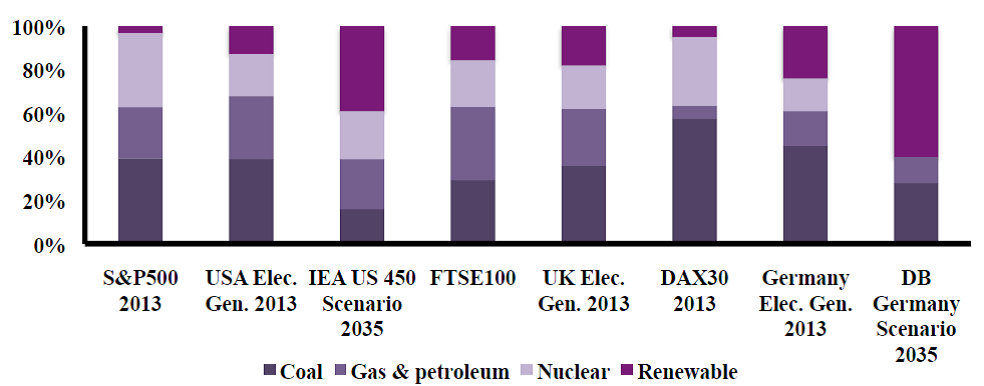

The utility sector is arguably the most interesting sector to analyze at energy-technology level because here there is a true competition between high-carbon and low-carbon technologies. At the same time, the analysis is complicated by the fact that it is challenging to measure the fuel mix of the listed equity universe the index is intended to represent. As a result, the analysis compares the electric utilities in the indices to the electricity mix of the economy. The analysis is limited to the FTSE 100, the DAX 30, and the S&P 500.

The results suggest that listed equity indices do not overweight high-carbon fuels relative to the generation of electricity. At the same time, the S&P 500 and DAX 30 underweight renewable energy, by 10% and 19%, respectively (Figure 5). This suggests significant suboptimal diversification. Interestingly, while the FTSE 100 is the worst performer in terms of exposure to the oil and gas sector, it is the best performer for the utility sector, with a well-diversified fuel mix. The fuel mix is weighted by electricity generation and not by the share of the companies in the index. Accordingly, it will be intriguing to see what these figures mean for fuel oil distributors. With studies suggesting that fuel is still not distributed evenly around the world, the impact that these trends will have on industrial fuel manufacturing should emerge over time.

Figure 5: Comparison of Index Electricity Generation with Economy and Scenarios

Source: Authors, based on US EIA data, annual reports, U.K. DECC, Bundesnetzagentur, and Deutsche Bank 2012.

Beyond diversification relative to the current economy, a key question, naturally, is: What will the trajectory be? To date, the annual reports of companies and the relevant databases do not provide a breakdown of capital expenditure of utilities by energy technology. As a result, it is currently impossible for investors to measure their diversification, or exposure, to the future. While the data is missing, the trajectory is clear. Scenarios suggest a significant increase in green technologies for both the German and U.S. electricity sectors. As outlined above, the analysis is not “clean” because it does not compare the fuel mix of the index with the fuel mix of the listed equity universe. In the United States, this is likely to be relevant with regard to electricity generation by public agencies like the Tennessee Valley Authority, which is not listed on the U.S. stock market. In Germany, renewable power generated by households or by municipalities is similarly not captured. While this may balance the results somewhat, it is unlikely to explain the 10% and 19% divergences, respectively. Moreover, it does not address the larger risk to the utility business model that may result from the broad “greening” of electricity generation.

The benchmarks used so far to analyze the diversification of cap-weighted equity indices at sector level were related to the listed equity universe. At subsector level, this standard was somewhat loosened, for it can be argued that exposure to the sector achieved through equity markets is largely designed to mirror the diversification of the sector. In any event, it seems unlikely that any bias within a sector is managed and actively counterbiased at portfolio level. It should be said in advance that the comparison of equity indices to the real economy is not a fair comparison. They are not built to mirror the real economy. Nevertheless, it is a helpful exercise when thinking about diversification. To demonstrate the relationship between the equity index and the economy, this study looks at the share of the oil and gas sector in the United States and the United Kingdom, the only two national geographies that have significant domestic upstream oil and gas exploration and production. The disconnect between these two metrics is apparent (Figure 6).

Figure 6: Index Diversification Compared to Listed Equity Universe and Economy

(Source: Authors, based on index factsheets, Damodaran 2014, U.K. ONS data, and US BEA data.

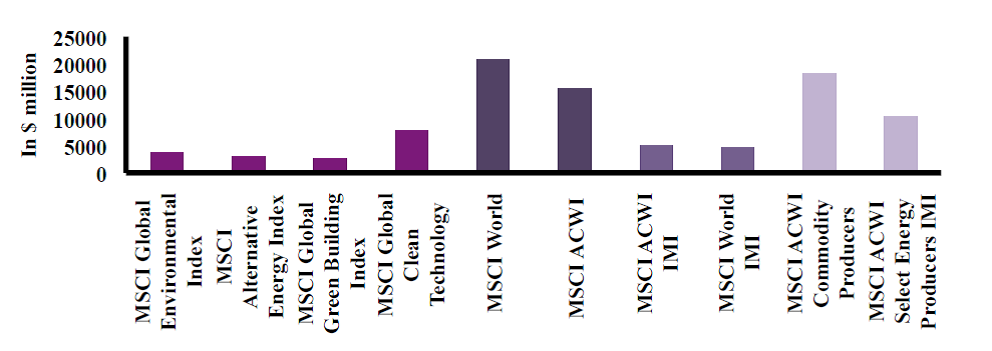

The underweighting of green technologies is likely to be a function of the size bias of market capitalization-weighted indices. Given the emerging nature of many climate-friendly industries and technologies, and the less-concentrated nature of these industries (for example, the renewable energy sector), they are likely to be less prominent among the largest companies in the market, compared to concentrated high-carbon sectors (Figure 7).

Figure 7: Average Market Capitalization of MSCI Cap-Weighted, Investable Universe, and Thematic Indices

Source: Authors, based on MSCI index factsheets.

Conclusions

The previous analysis suggests a diversification bias of cap-weighted equity indices. While there is some uncertainty about the degree of diversification bias, by default given varying measures of optimal diversification, the analysis shows relatively conclusively the presence of this bias across indices, at sector level or energy-technology level or at both levels. As a result, passive investors and active investors using these indices as sector allocation guidelines expose themselves to asset-specific risk that is not hedged in the equity share of the portfolio. This analysis adds to the growing literature on the shortcomings and challenges of index investing, both in terms of the different types of biases (for example, geography, size, and so on), and the new types of risks that appear as index investing grows. It also suggests that, while divestment would indeed lead to reduced diversification, current diversification strategies also don’t appear optimal, particularly given the likely transition to a low-carbon economy.

The analysis shows that investors replicating these indices (in whichever form) make an implicit bet on a certain type of future-a future represented by the index’s constituents. Crucially, the question then is not whether betting on such a future is risky or not, but rather the extent to which this implicit bet, not properly identified in nonclimate specific sector breakdowns of indices, is an explicit part of the investors’ strategy.

The study thus suggests that in the context of the energy transition, it no longer suffices to aim for a diversified exposure to sectors-investors also need to manage their exposure to energy technologies within sectors. The relevant metrics, then, are not only related to current diversification (such as installed capacity for the utility sector), but also to the forward-looking exposure of companies, particularly apparent in their capital expenditure decisions.

Acknowledgments

The authors would like to thank Allianz Global Investors and HSBC for the financial support in realizing the research. The authors would also like to thank MSCI ESG Research and Morningstar for providing data. Finally, the authors would like to thank Gabriel Thoumi, CFA, for support in reviewing the document and contributing to its final iteration.

References

Bachelier, L. 1900. “Theorie de la Speculation.” Annales Scientifiques de l’Ecole Normale Superieure 3(17): 21–86.

Barber, B. M., and J. D. Lyon. 1997. “Firm Size, Book-to-Market-Ratio, and Security Returns.” Journal of Finance 52(2): 875–883.

Basu, S. 1977. “Investment Performance of Common Stocks in Relation to Their Price-Earnings Ratio: A Test of the Efficient Market Hypothesis.” Journal of Finance 32(3): 663–682.

Bhandari, L. C. 1988. “Debt/Equity Ratio and Expected Stock Returns: Empirical Evidence.” Journal of Finance 43(2): 507–528.

Black, F. 1972. “Capital Market Equilibrium with Restricted Borrowing.” Journal of Business 45(3): 444–455.

Black, F., M. C. Jensen, and M. Scholes. 1972. “The Capital Asset Pricing Model: Some Empirical Tests.” In Studies in the Theory of Capital Markets, M. Jensen. New York: Praeger.

Chan, L. C., N. Jegadeesh, and J. Lakonishok. 1995. “Evaluating the Performance of Value Versus Glamour Stocks: The Impact of Selection Bias.” Journal of Financial Economics 38(3): 269–296.

Clare, A. N. Motson, and S. Thomas. 2013. “An evaluation of alternative equity indexes.” Part 1: Heuristic and Optimised Weighting Schemes.” Cass Business School.

Cremers, Matijn, and Antii Petajisto. 2013. “Active Share and Mutual Fund Performance.” Financial Analysts Journal Volume 69.

Coeurdacier, Nicolas, and Helene Rey. 2011. “Home Bias in Open Economy Financial Macroeconomics.” NBER Working Paper No. 17691.

DAX. 2014. “DAX Index Factsheet.”

Dobbs, Richard, et al. 2010. “Farewell to Cheap Capital: The Implications of Long-term Shifts in Global Investments and Savings.” McKinsey Global Institute.

Energy Information Administration. 2014. “Electricity Data.”

Ernst and Young. 2012. “Performance measurement in the banking industry-post-crisis trends.”

Fabozzi, Frank J., Francis Gupta, and Harry M. Markowitz. 2002. “The Legacy of Modern Portfolio Theory.” Journal of Investing Fall 2002.

Fama, E. F. 1965. “The Behavior of Stock Market Prices.” Journal of Business 38(1):

34–105.

Fama, E. F., and K. R. French. 1993. “Common Risk Factors in the Returns on Stocks and Bonds.” Journal of Financial Economics 33(1): 3–56.

Fama, E. F., and K. R. French. 1996. “Multifactor Explanation of Pricing Anomalies.” Journal of Finance 51(1): 55–84.

Fama, E. F., and K. R. French. 2004. “The Capital Asset Pricing Model: Theory and Evidence.” Journal of Economic Perspectives 18(3): 25–46.

Fama, E. F., and J. D. Macbeth. 1973. “Risk, Return and Equilibrium: Empirical Tests.” Journal of Political Economy 81(3): 607–636.

Fidelity. 2013. “Benchmarking, Better Beta and Beyond.”

FTSE. 2014. “FTSE 100 Factsheet.”

Gerlach, Jeffrey R. 2005. “Imperfect Information and Stock Market Volatility.” Financial Review Vol. 40(2): 173–194.

Graham, B., and D. Dodd. 1934. Security Analysis. New York: McGraw-Hill.

Ibbotson SBBI 2009 Classic Yearbook. Chicago: Morningstar.

International Energy Agency (IEA). 2014. World Energy Outlook: Special Report Investments. Paris: IEA Publications.

Jegadeesh, N., and S. Titman. 1993. “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.” Journal of Finance 48(1): 435–454.

Jorgensen, Dale. 1967. “The Theory of Investment Behavior” In Determinants of Investment Behavior, edited by Rober Feber. NBER Books: 129–188.

Markowitz, H. M. 1952. “Portfolio Selection.” Journal of Finance 7(1): 77–91.

McKinsey Global Institute. 2014. “Global Financial Assets.”

MSCI. 2014. “Investor Briefing.” MSCI Briefing at 2° Investing Initiative and MSCI Workshop in New York City, February 25, 2014.

MSCI. 2014a. “MSCI World Fact Sheet.”

Nicholson, S. F. 1960. “Price-Earnings Ratio.” Financial Analysts Journal 16(4): 43–45.

Osborne, M. F. 1959. “Brownian Motion in the Stock Market.” Operations Research 7(2): 145–173.

Petajisto, Antti. 2013. “Active share and mutual fund performance.” Financial Analysis Journal 69(4): 73-93.

PriceWaterhouse Coopers (PwC). 2014. Asset Management 2020: A Brave New World.

Rosenberg, B., K. Reid, and R. Lanstein. 1985. “Persuasive Evidence of Market Inefficiency.” Journal of Portfolio Management 11(3): 9–17.

Ross, S. 1976. “The Arbitrage Theory of Capital Asset Pricing.” Journal of Economic Theory 13(3): 341–360.

Samuelson, P. 1965. “Proof That Properly Anticipated Prices Fluctuate Randomly.” Industrial Management Review 6(2): 41–49.

Sharpe, W. F. 1964. “Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk.” Journal of Finance 19(3): 425-442.

Stoxx. 2014. “Stoxx 600 Factsheet.”

S&P 500. 2014. “S&P 500 Factsheet.”

Tobin, J. 1958. “Liquidity Preferences as Behavior Towards Risk.” Review of Economic Studies 25(2): 65-86.

UNEP Fi. 2013. “Investor Briefing-Carbon Portfolio.”

U.K. Office for National Statistics. 2014. “Data.”

U.S. Bureau of Economic Analysis (BEA). 2014. “National Economic Accounts.”

Vanguard. 2013. “Tax Efficiency: A Decisive Advantage for Index Funds.”

Vanguard. 2014. “Principle 3: Minimize Cost.”

Vardharaj, Raman, Frank J. Fabozzi, and Frank. J. Jones. 2004. “Determinants of Tracking Error for Equity Portfolios.” Journal of Investing 13(2): 37–47.

Vernimmen. 2014. “Smart Beta.”

World Economic Forum. 2012. Measurement, Governance and Long-term Investing. New York: World Economic Forum USA; Switzerland: World Economic Forum.

Williams, J. B. 1938. The Theory of Investment Value. Amsterdam: North Holland.

Appendix 1:

The “active sector share” of funds was calculated based on the following equation:

with equal to the weight of the sector i in the fund and equal to the weight of the same sector in the fund’s benchmark index, in this case the MSCI World. The calculation is based on Morningstar fund data from January 2014. The calculation was performed based on 10 sectors. The methodology is based on Petajisto (2013) in his work on the active share-the difference is the focus on sectors as opposed to stocks. Results are presented both in terms of assets under management (AUM) and number of funds.

Example: If the share of oil and gas in the fund is 12% and the share is 10% in the index, the absolute difference is 2%. If the absolute difference for all sectors is 2%, the fund has an active share of 10%.

To control for funds with factor bets or concentrated stock picking, the authors excluded funds from the sample that diverge more than 10% from any one sector, and a sample excluding funds that diverge more than 5% from any one sector.

Biographies

Jakob Thomae currently works as the Program Manager for the 2° Investing Initiative (2°ii). He is the author and co-author of a number of studies, including those on the topics of stress-testing long-term and carbon risks, artificial short-termism, the role of financial regulatory policies in shifting private capital to climate-friendly investments, and financed emissions methodologies. Jakob is currently pursuing his PhD at the Conservatoire National des Arts et Métiers on the implications of climate change for financial portfolios.

Stanislas Dupré initiated the 2° Investing Initiative and now serves as its Global Director.

Manuel Coeslier – Manuel Coeslier is an analyst with 2° Investing Initiative and Mirova. He is currently pursuing his PhD on climate performance metrics for companies at Ecole Centrale de Nantes, Audencia School of Management.

Alexandre Gorius is a graduate student from Paris Dauphine University. For 2° Investing Initiative, he has contributed research on tax incentives on savings interest and the use of benchmark indices by investors.

Danyelle Guyatt is Managing Director of Collaborare Advisory, a research and advisory company that is dedicated to promoting long-term sustainable investment. Danyelle completed a PhD on the behavioral impediments to long-term responsible investing, and over the years have held various positions in academia, investment consulting, and funds management.

[1]. Private equities and real estate assets, probably representing by far the largest asset classes, are excluded.

[2]. While CCS may play a major role in the oil and gas sector in the future, it does not appear prominent today.